HOME >> BUSINESS

China uncovers $10b worth of falsified trade

By Song Shengxia Source:Global Times Published: 2014-9-25 23:53:01

Companies forging transactions for arbitrage, says SAFE

A ship downloads containers in Qingdao Port on Thursday. Photo: CFP

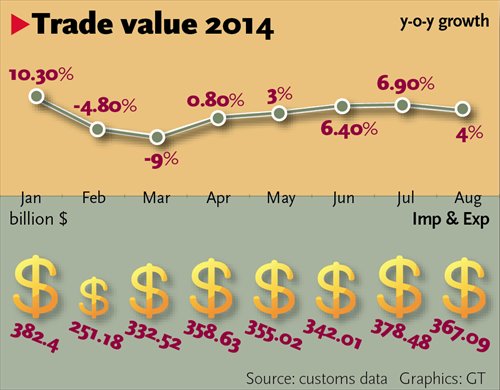

Trade value 2014

China has reported almost $10 billion of falsified trade transactions nationwide after an extensive investigation into false trade launched last April, an official with the country's foreign exchange regulator said Thursday.

Many companies forge, alter, and reuse trade documents to create artificial transactions to turn transship trade into a speculative arbitrage tool, Wu Ruilin, a deputy head for foreign exchange management and inspection under the State Administration of Foreign Exchange (SAFE), said at a press conference on Thursday.

Since last April, the administration has found nearly $10 billion of such fraud, including the Qingdao Port fraud, throughout the country and handed 15 cases over to the police, according to Wu.

"Fake trade has increased pressure of hot money inflows and provides illegal channels for criminals to move capital in and out of the country," Wu said.

China has launched a crackdown since April 2013 on fake export invoices used for disguising cross-border capital flows , after some importers and exporters were found to forge trade transactions in order to bypass China's strict capital controls and move capital in and out of the country.

Some banks failed to fulfill their duties to check the authenticity of trade documents, which helped aggravate the fraudulent behavior, Wu said.

The regulator started a crackdown in 13 cities in 2013 and has extended the investigations to 24 provinces and cities including Qingdao where people involved in the Qingdao Port frauds have also been probed, according to Wu.

The regulator will severely punish the irregular practices and hand offenders to the police, Wu said.

The Qingdao Port, operator of a bonded warehouse at the world's seventh-busiest port by cargo throughput in East China's Shandong Province, has been at the center of an ongoing fraud investigation.

Decheng Mining, a local private metals trading firm, is being investigated after it was reported in early June to have duplicated warehouse certificates in order to repeatedly obtain multiple bank loans.

Qingdao Port International Co, the operator of Qingdao Port, did not answer calls for comment Thursday.

A staff member at the general office of the Qingdao Financial Work Office told the Global Times Thursday that the case is under investigation in accordance with regular proceedings, without giving further details.

On September 12, Qingdao Port International Co said in a statement that an alleged financing fraud at Qingdao Port involved about 300,000 tons of alumina, 20,000 tons of copper and as much as 80,000 tons of aluminum ingots, according to a Reuters report.

"Compared with the total trade volume, $10 billion in falsified trade transactions is not a large sum. But the Qingdao case has definitely prompted banks to tighten their control on trade financing and issuance of letters of credit," Zhang Sida, a nonferrous metals analyst with Shanghai Continent Futures, told the Global Times.

Industrial and Commercial Bank of China (ICBC), one of the many banks including HSBC and Standard Chartered that have been affected by the case, said in August that the bank had accumulated no more than $200 million in bad loans from the suspected fraud at Qingdao Port. ICBC did not answer calls for comment by press time.

"A transaction information disclosure platform involving banks, ship owners, warehouse document management companies as well as regulators should be set up to strengthen warehouse document management procedures," Lu Hongjun, president of the Shanghai Institute of International Finance, told the Global Times Thursday.

Posted in: Industries